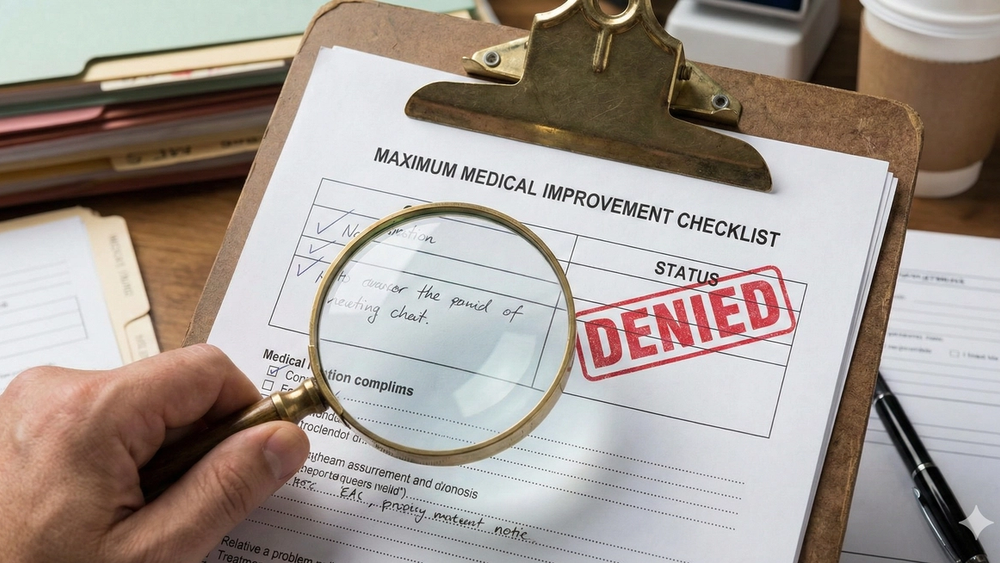

What Is Maximum Medical Improvement (MMI)?

In the world of personal injury law across the United States, Maximum Medical Improvement (MMI) is a critical milestone. It represents the point where a medical professional determines that an injured party’s condition has stabilized and is unlikely to improve further, even with additional treatment. Reaching MMI does not necessarily mean you are "healed" or back to your pre-accident self; rather, it means your recovery has plateaued. For insurance adjusters, this is traditionally the earliest point they are willing to discuss a final settlement figure because it allows them to calculate permanent impairment ratings and future medical costs with certainty. However, in 2025, we are seeing a trend where this medical term is being weaponized as a procedural stop-sign to stall negotiations indefinitely.

The 2025 Inflation Strategy: Why Delay Pays the Insurer

The economic landscape of 2025 has incentivized insurance carriers to hold onto their cash reserves for as long as possible. With fluctuating inflation rates impacting the real value of the dollar, paying out a $50,000 settlement today costs a carrier "more" in real terms than paying it out 18 months from now. Consequently, adjusters are under stricter internal mandates to delay payouts until the absolute last moment. By insisting on waiting for a formal MMI declaration—even in cases where injuries are clearly defined—adjusters can push settlements into the next fiscal quarter or year. This "financial drag" tactic allows them to earn interest on the money that should be in your pocket, effectively profiting from your wait.

Affected by a Medical Malpractice Issue?

Our specialized tool can help you estimate the potential worth of your case based on current laws and precedents.

Weaponizing "Subjective" Recovery Timelines

A growing tactic we have observed nationwide, from Florida to California, involves adjusters disputing when MMI has actually been reached. In 2025, sophisticated claims software is increasingly used to flag "excessive treatment duration." If your recovery takes two months longer than their algorithm predicts, the adjuster may claim you haven't truly reached MMI or that your ongoing symptoms are unrelated to the accident. This forces claimants into a cycle of scheduling additional independent medical exams (IMEs) to prove their status. This bureaucratic loop serves a dual purpose: it delays the check and wears down the claimant psychologically, making them more likely to accept a lower "lowball" offer just to end the process.

Navigating State Statutes and MMI Delays

It is vital to understand how MMI delays interact with your state's Statute of Limitations. Whether you are in Texas with a two-year limit or Maine with a six-year limit, the clock is always ticking. Insurance adjusters are well aware of these deadlines and may drag out the MMI determination process until you are uncomfortably close to the filing deadline. If you are still treating and haven't reached MMI as the statute date approaches, you may be forced to file a lawsuit to preserve your rights, which increases legal costs and stress. Understanding the true value of your case early on—before MMI is even fully established—is the best defense against these stalling tactics.

How to Counteract Delays and Estimate Value Now

You do not have to wait for an adjuster's permission to understand what your injury claim is worth. While MMI provides a precise medical endpoint, experienced legal tools can project case values based on current treatment trajectories and similar nationwide verdicts. By using an independent case evaluation estimator, you gain leverage. You can demonstrate to the adjuster that you know the fair market value of your claim, regardless of their stalling tactics. If an insurer is hiding behind MMI to withhold payment, knowing your numbers is the first step in forcing them to the negotiation table.

Want to know what your case is worth?

Leave your name and number — find out free in two minutes, no obligation.

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. For specific legal guidance regarding your situation, please consult with a qualified attorney.